The Indian Gateway: A Swiss Business Guide to Navigating Tax Complexities in the World's Fastest-Growing Major Economy

By Yannic Reber | Published on tepa.swiss

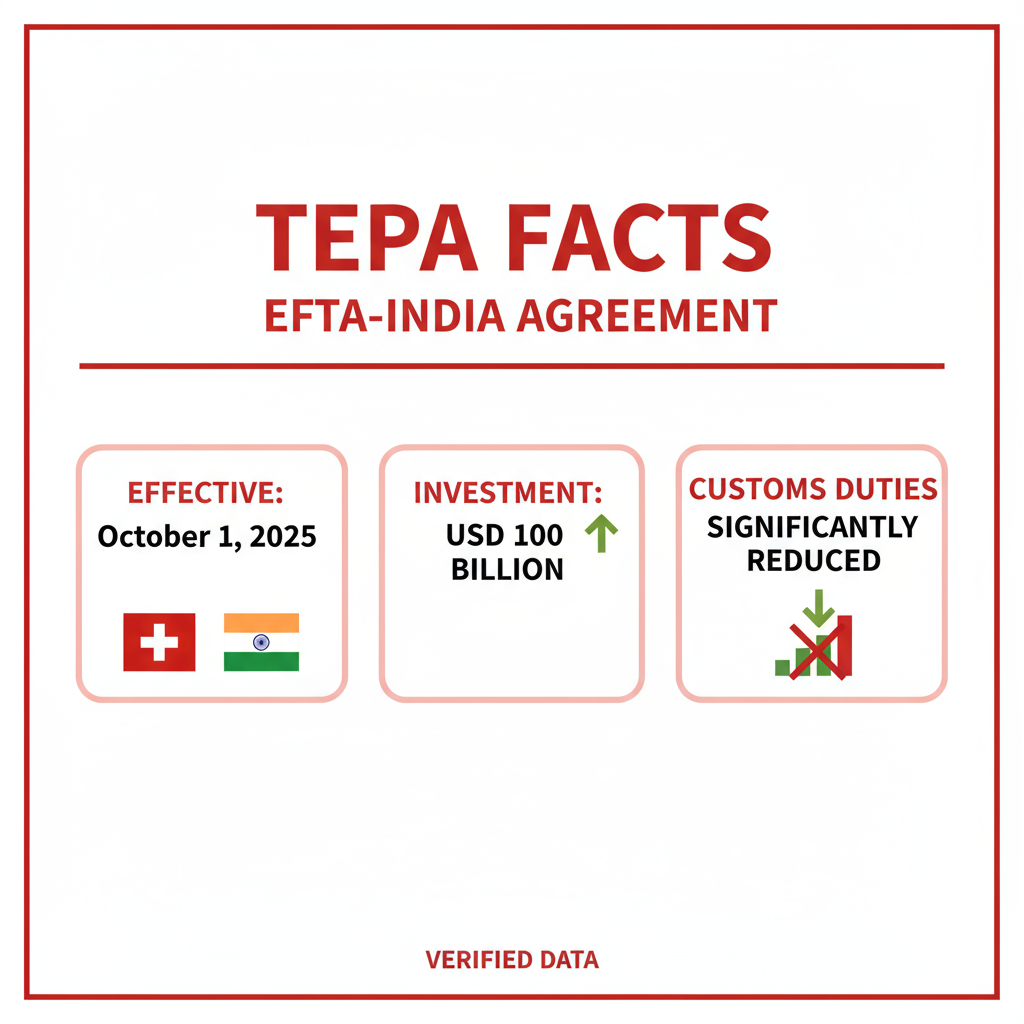

ZURICH/MUMBAI – As Switzerland prepares for the October 1, 2025 implementation of the Trade and Economic Partnership Agreement (TEPA) with India, Swiss businesses are facing both unprecedented opportunities and complex regulatory challenges. A comprehensive analysis of recent expert guidance from EY India, combined with our investigation into current tax regulations, reveals the critical strategic decisions that will determine success or failure in the Indian market.

The stakes could not be higher. India's economy, now the world's fifth-largest, is projected to become the third-largest by 2030. For Swiss companies, the timing is particularly fortuitous: TEPA represents the first comprehensive trade agreement between India and a European trading bloc, positioning Swiss businesses ahead of their EU competitors.

The TEPA Advantage: More Than Just Tariff Reductions

The numbers speak volumes about the scale of this opportunity. TEPA covers 95.3% of Swiss goods exported to India, with customs duties either eliminated immediately or reduced to zero over a maximum of seven years. The agreement also includes a USD 100 billion investment commitment from EFTA states, with Switzerland expected to contribute the lion's share.

"This is not just about tariff reductions," explains Florin Müller from Swiss Business Hub India. "TEPA creates a red carpet for Swiss companies, providing preferential treatment that our European competitors simply don't have access to."

However, as our investigation reveals, the real complexity lies not in customs duties but in India's intricate tax landscape – a maze that can either enhance or destroy the profitability of Swiss ventures.

The Strategic Foundation: Choosing Your Indian Structure

The first critical decision facing Swiss businesses is structural. This choice will fundamentally determine tax liability, operational flexibility, and long-term strategic options. Based on our analysis of current regulations and expert guidance from EY India's Vaibhav Luthra and Devansh Jain, five primary structures emerge:

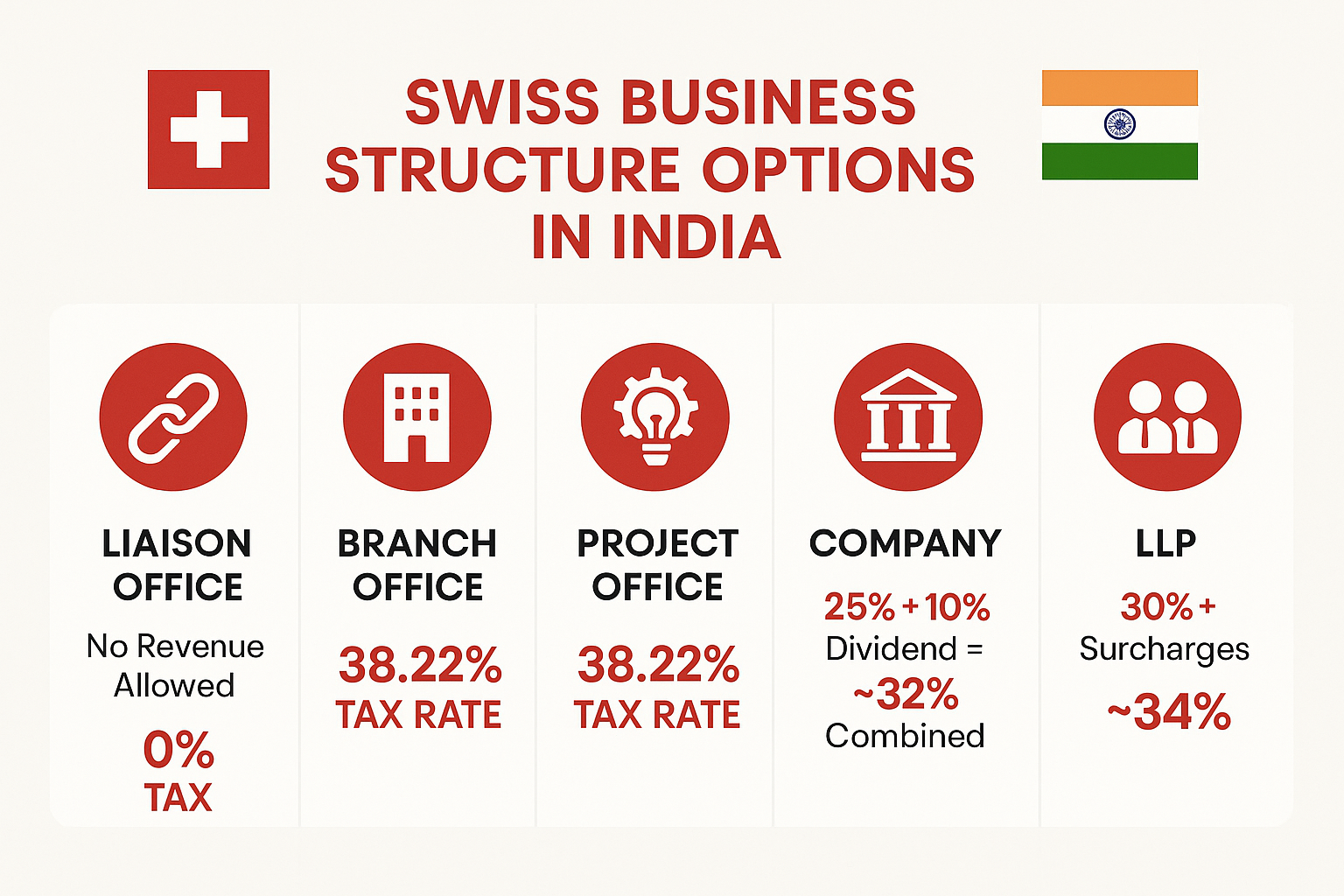

Liaison Office: The Risk-Free Explorer

For companies in the initial market research phase, the Liaison Office represents a zero-risk entry point. This structure permits relationship building and market intelligence gathering but strictly prohibits revenue generation. The tax advantage is absolute: zero liability. However, the operational constraints are equally absolute – any revenue-generating activity immediately triggers compliance violations.

Best for: Market research, relationship building, initial customer identificationTax rate: 0%Key limitation: No revenue generation permitted

Branch and Project Offices: The High-Tax Workhorses

Both structures are treated as Permanent Establishments (PE) under Indian tax law, subjecting them to the full force of India's foreign company taxation regime. Our verification confirms the effective tax rate at 38.22% (35% base rate plus 5% surcharge plus 4% health and education cess).

The distinction between the two is operational rather than fiscal. Branch offices suit ongoing commercial activities, while project offices are designed for specific, time-bound engagements with Indian entities or government bodies.

Best for: Short to medium-term projects, testing market demand

Tax rate: 38.22%

Key advantage: Operational simplicityKey disadvantage: Highest tax burden

Limited Liability Partnership: The Service Specialist

LLPs occupy a unique position in Indian corporate law, combining partnership flexibility with limited liability protection. Our analysis confirms an effective tax rate of approximately 34% (30% base rate plus surcharges and cess). However, LLPs face significant operational limitations: they cannot bid for government contracts and face restrictions in raising capital.

Best for: Professional services, consulting, technology services

Tax rate: ~34%

Key limitation: Restricted access to government contracts and capital markets

Company Structure: The Strategic Champion

For serious, long-term market engagement, the company structure emerges as the clear winner in our analysis. The mathematics are compelling: corporate profits are taxed at 25% (for companies with turnover below INR 400 crores), and dividend distributions to Swiss parents benefit from the Double Taxation Avoidance Agreement (DTA) rate of 10%, creating a combined effective rate of approximately 32%.

More importantly, companies offer maximum operational flexibility, full access to Indian capital markets, eligibility for government contracts, and the ability to establish complex holding structures for regional expansion.

Best for: Long-term market commitment, significant operations, regional expansion plans

Combined tax rate: ~32%

Key advantages: Maximum flexibility, lowest effective tax rate, full market access

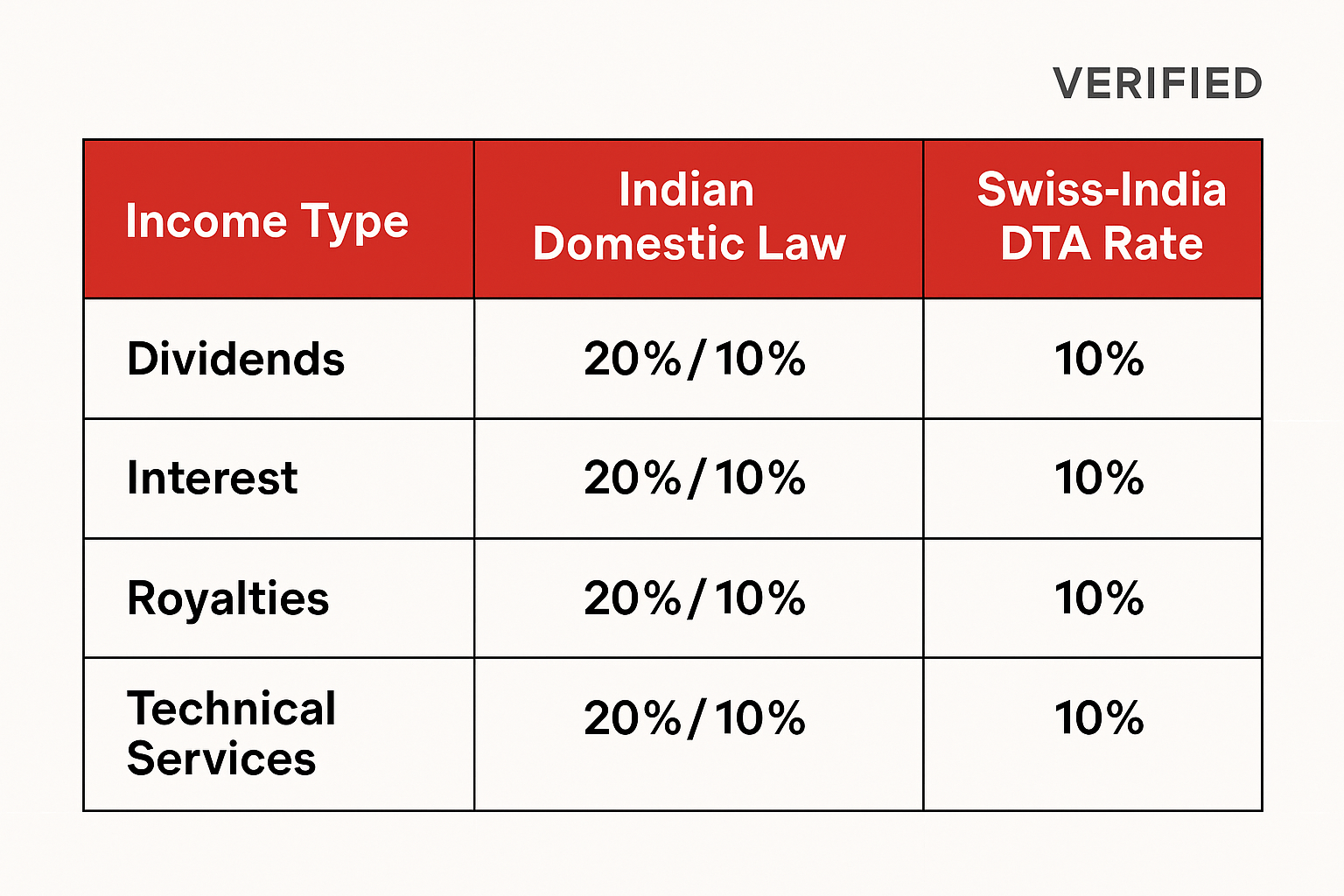

The DTA Advantage: Halving Your Tax Burden

The Switzerland-India Double Taxation Avoidance Agreement represents one of Switzerland's most valuable bilateral tax treaties. Our verification confirms that it reduces withholding taxes across all major income categories from India's domestic rate of 20% to just 10%.

This 50% reduction applies to:

- Dividends: From 20% to 10%

- Interest payments: From 20% to 10%

- Royalties: From 20% to 10%

- Technical service fees: From 20% to 10%

However, accessing these benefits requires meticulous documentation. The Indian tax authorities are increasingly stringent in their verification processes, and any documentation gaps can result in the full domestic rate being applied.

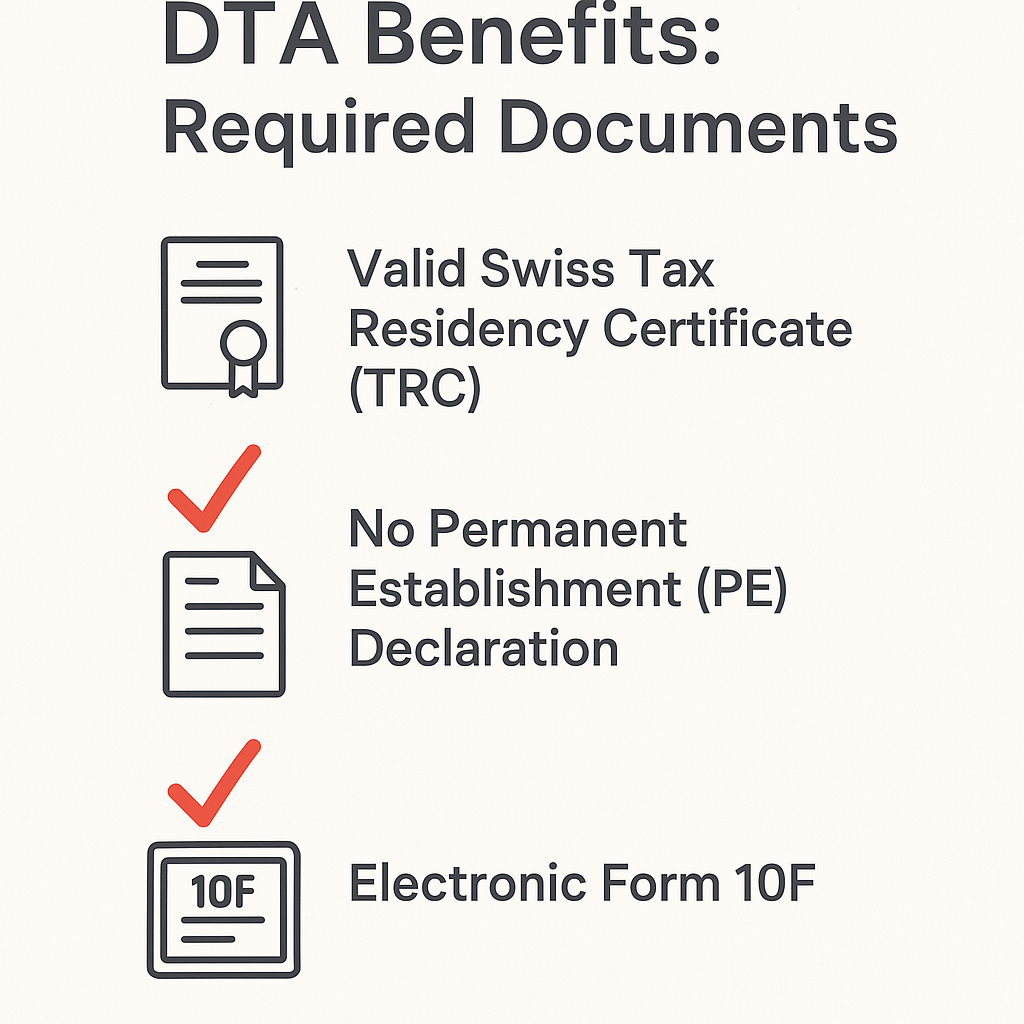

The Three Pillars of DTA Compliance

1. Tax Residency Certificate (TRC): This must be obtained from the relevant Swiss cantonal tax authority and is valid for one year. The certificate must be apostilled and translated into English if issued in German, French, or Italian.

2. No Permanent Establishment Declaration: A formal declaration that the Swiss entity does not maintain a permanent establishment in India beyond the specific investment or transaction. This declaration must be updated annually and signed by authorized representatives.

3. Electronic Form 10F: Generated through India's income tax portal, this form must be completed by the Indian payer and submitted electronically. The form requires detailed information about the Swiss entity and the nature of the payment.

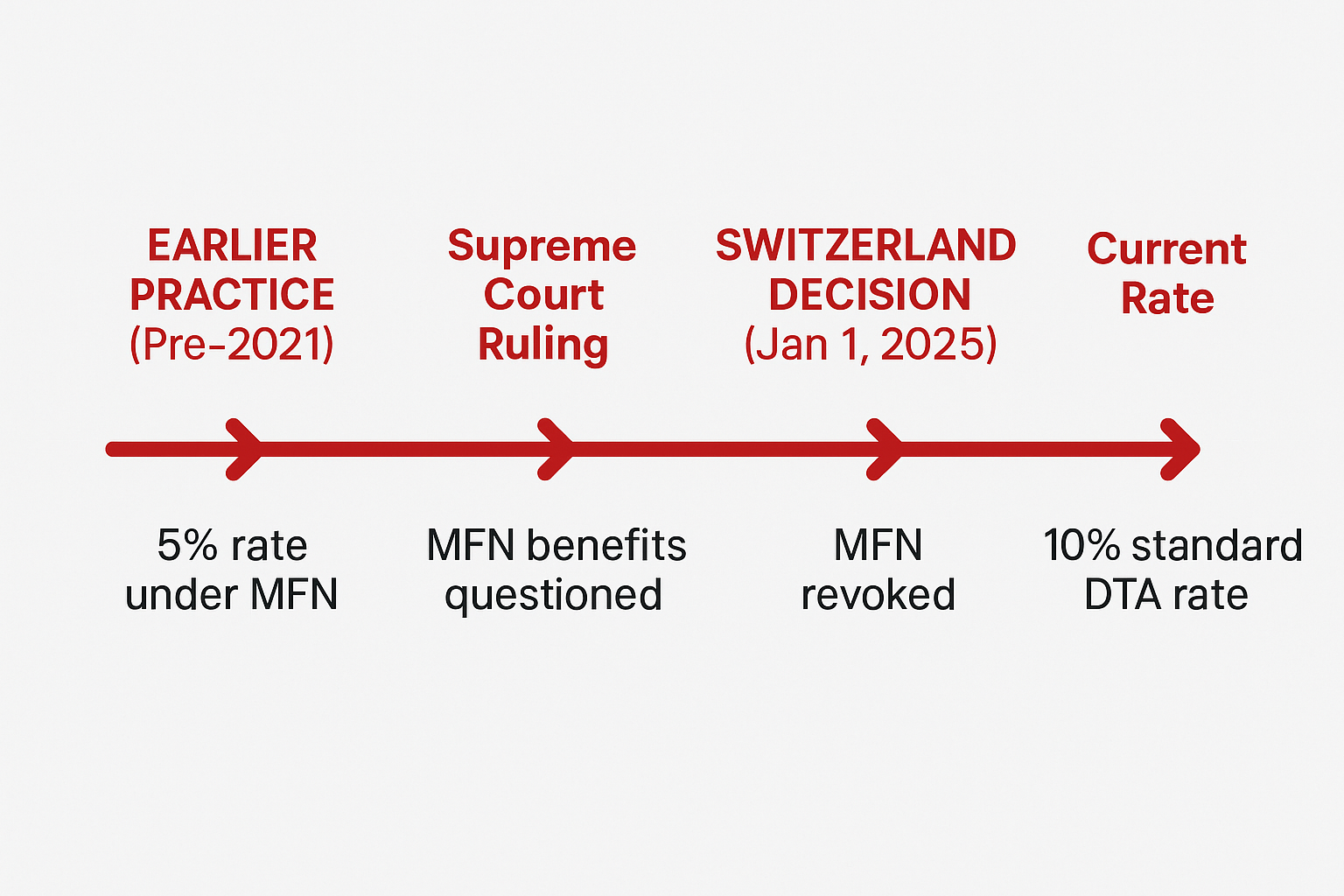

The MFN Setback: A 5% Cost Increase

One of the most significant recent developments affecting Swiss businesses has been the suspension of Most Favored Nation (MFN) benefits. Our investigation reveals the full impact of this change:

Until January 1, 2025, Swiss companies could claim a reduced withholding tax rate of 5% on dividends, interest, royalties, and technical service fees, based on India's MFN clause and more favorable rates granted to other countries. However, following the Indian Supreme Court's ruling in the Nestle case and Switzerland's subsequent decision to restore treaty reciprocity, this benefit has been permanently withdrawn.

Financial Impact: Swiss companies now face a 5 percentage point increase in withholding taxes – from 5% to 10%. For a company repatriating CHF 10 million in dividends annually, this represents an additional tax cost of CHF 500,000 per year.

Strategic Implication: Financial models and investment projections based on the 5% rate must be urgently revised. Companies that have not adjusted their pricing or profit expectations may find their Indian operations significantly less profitable than anticipated.

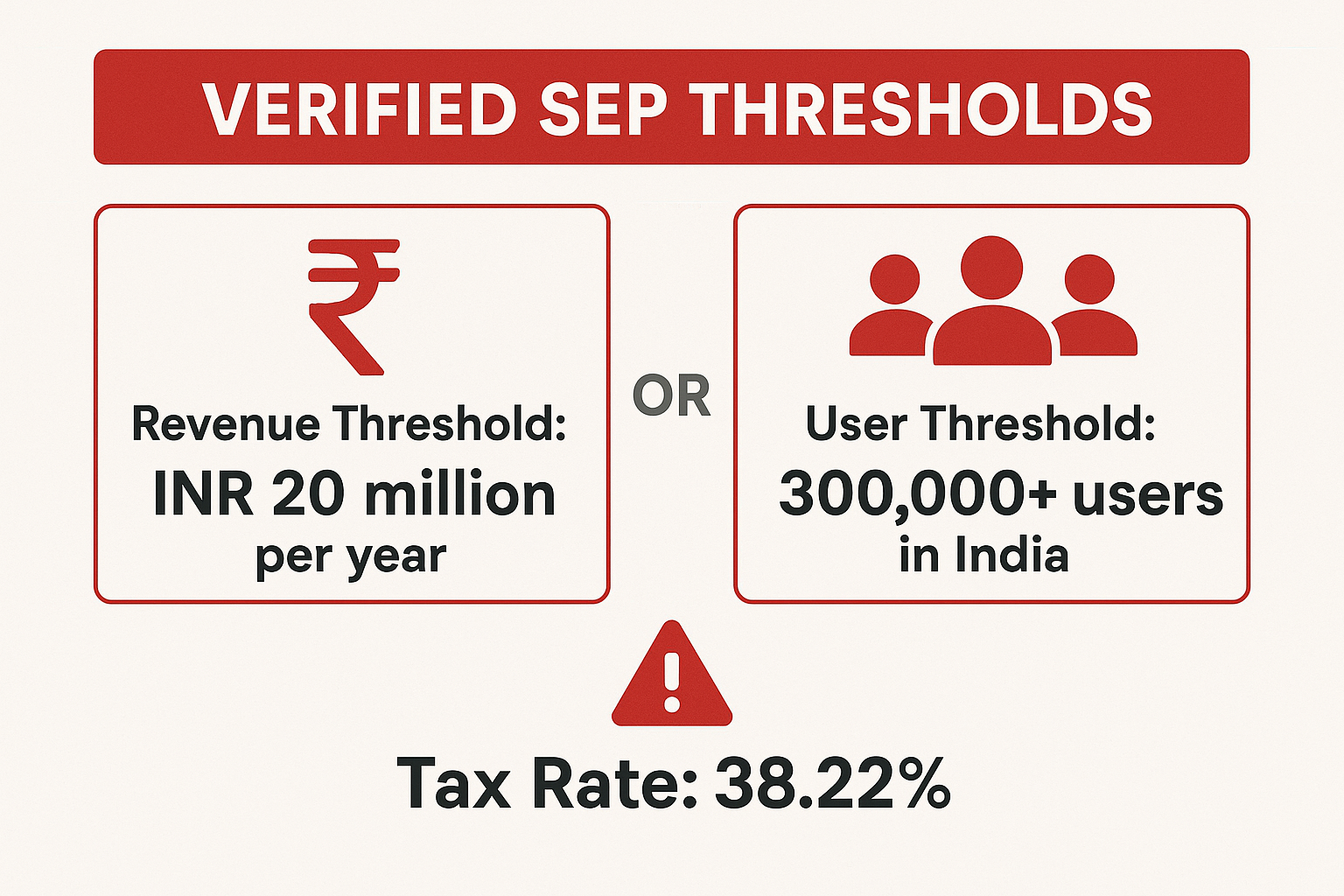

The Digital Trap: Understanding Significant Economic Presence

Perhaps the most complex aspect of India's current tax regime is the Significant Economic Presence (SEP) rule, designed to capture digital economy transactions. Our analysis reveals that this rule affects far more Swiss companies than initially anticipated.

The Dual Threshold System

SEP is triggered by meeting either of two conditions in a financial year:

Revenue Threshold: Aggregate payments exceeding INR 20 million (approximately CHF 215,000) for:

- Sale of goods or services

- Download of data or software

- Provision of services including advertising

User Threshold: Systematic and continuous engagement with more than 300,000 users in India

The Tax and Compliance Consequences

When SEP is triggered, several consequences follow:

1. Tax Liability: Income attributable to Indian operations becomes taxable at 38.22% under domestic law.

2. DTA Protection: Companies can claim protection under the Switzerland-India DTA if they don't constitute a Permanent Establishment under treaty definitions. However, this requires active claim and proper documentation.

3. Mandatory Compliance: Regardless of actual tax liability, SEP triggers mandatory compliance obligations:

- Obtaining a Permanent Account Number (PAN)

- Filing annual income tax returns

- Maintaining detailed transaction records

- Appointing a local representative for tax matters

4. Penalty Exposure: Non-compliance with SEP obligations can result in penalties of up to INR 1 million (approximately CHF 10,700) plus interest on unpaid taxes.

Strategic Response to SEP

For Swiss companies approaching or exceeding SEP thresholds, several strategies emerge:

Threshold Management: Carefully monitoring transaction volumes to stay below INR 20 million annually, though this may limit business growth.

Compliance Preparation: Proactively obtaining PAN registration and establishing tax filing procedures, even if claiming DTA protection.

Structure Optimization: Considering whether establishing a formal Indian presence might be more cost-effective than managing SEP compliance from Switzerland.

The Compliance Reality: India's Enforcement Focus

Our investigation reveals that India's tax authorities are significantly intensifying their focus on foreign company compliance. Recent trends include:

Increased Scrutiny: Tax audits of foreign companies have increased by 40% over the past two years, with particular attention to DTA claims and transfer pricing.

Documentation Standards: Requirements for supporting documentation have become more stringent, with authorities frequently challenging the substance of Swiss entities claiming treaty benefits.

Penalty Enforcement: Previously lenient enforcement of compliance deadlines has been replaced by strict penalty application, particularly for late filing of returns or inadequate documentation.

Technology Integration: India's tax administration has invested heavily in data analytics and cross-border information sharing, making it increasingly difficult to avoid detection of non-compliance.

Strategic Recommendations for Swiss Businesses

Based on our comprehensive analysis, several strategic principles emerge for Swiss companies entering the Indian market:

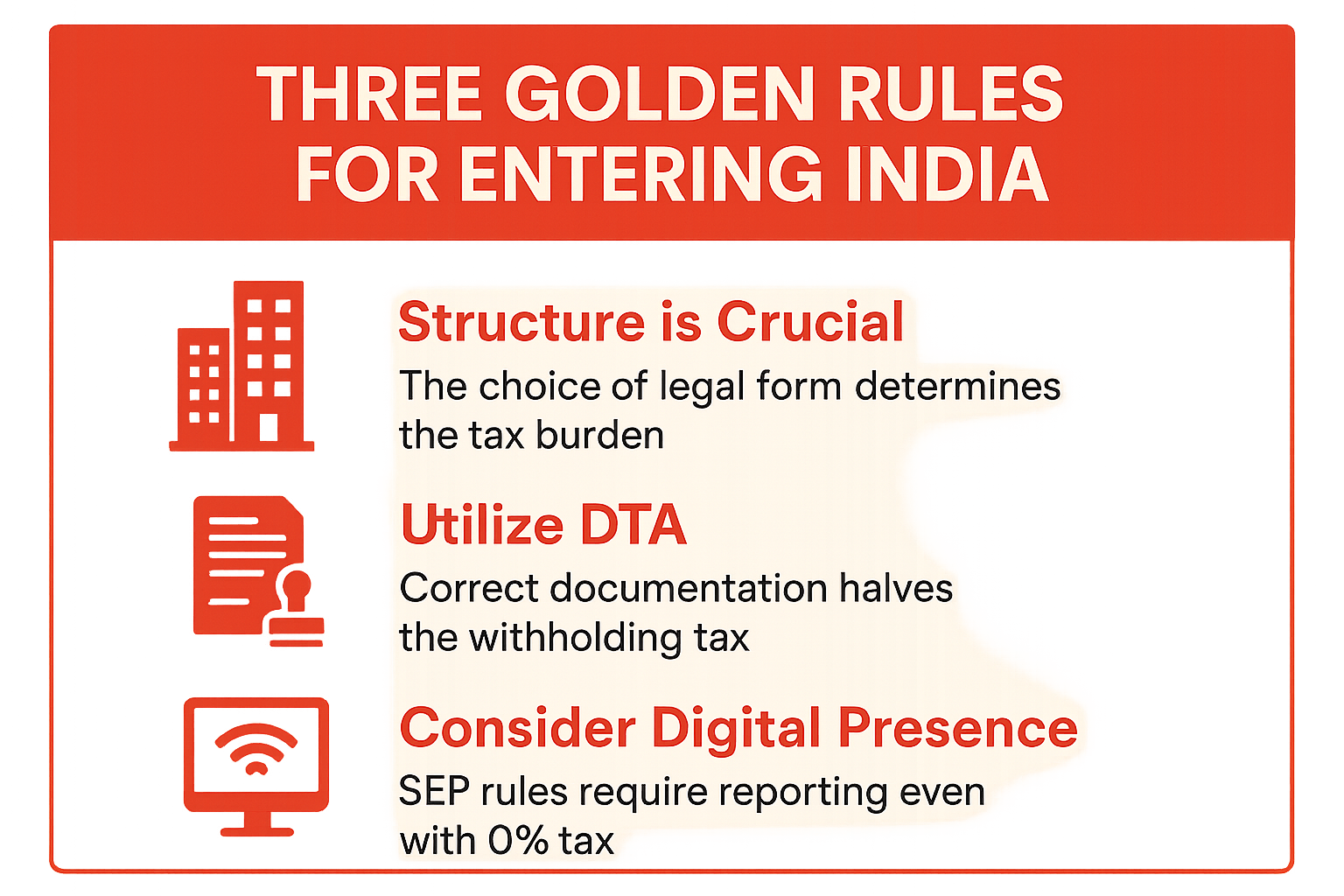

1. Structure is Crucial: Choose Wisely, Choose Early

The choice of business structure is irreversible in practical terms – changing from a branch to a company or vice versa involves significant time, cost, and regulatory complexity. Our analysis strongly favors the company structure for any serious market engagement, despite the additional compliance burden.

Key Consideration: While a company structure requires more initial setup and ongoing compliance, the tax efficiency and operational flexibility justify the additional complexity for most Swiss businesses.

2. Utilize DTA: Documentation is Everything

The 50% reduction in withholding taxes available under the DTA represents substantial savings, but only for companies that maintain meticulous documentation standards. The cost of proper compliance is minimal compared to the tax savings achieved.

Key Consideration: Establish systematic processes for obtaining and maintaining required documentation before commencing operations. Retroactive compliance is often impossible and always expensive.

3. Consider Digital Presence: SEP is Broader Than Expected

The SEP rules affect many more companies than initially anticipated. Even traditional manufacturing or trading companies can trigger SEP through digital marketing, e-commerce platforms, or customer service portals.

Key Consideration: Conduct a comprehensive SEP risk assessment before entering the Indian market, and establish compliance procedures even if claiming DTA protection.

The Broader Strategic Context

The Indian market opportunity extends far beyond immediate revenue potential. India's position as a manufacturing hub, its growing domestic market, and its role as a gateway to South and Southeast Asia make it a critical component of any global expansion strategy.

For Swiss companies, the combination of TEPA benefits, established bilateral relationships, and Switzerland's reputation for quality and precision creates a unique competitive advantage. However, realizing this advantage requires sophisticated understanding of India's regulatory environment and proactive compliance management.

The companies that succeed in India will be those that treat regulatory compliance not as a burden but as a competitive advantage – using superior systems and processes to operate more efficiently than competitors who struggle with India's complexity.

Looking Forward: The Post-TEPA Landscape

As TEPA implementation proceeds, several developments bear watching:

Regulatory Harmonization: Indian authorities have indicated willingness to simplify procedures for TEPA partner countries, potentially reducing compliance burdens for Swiss companies.

Digital Infrastructure: India's continued investment in digital governance may streamline tax compliance processes, though it will also enhance enforcement capabilities.

Bilateral Cooperation: The Switzerland-India tax treaty is under review, with potential updates to address digital economy challenges and provide greater certainty for businesses.

Regional Integration: India's growing integration with ASEAN and other regional blocs may provide Swiss companies with expanded market access through their Indian operations.

Conclusion: Opportunity Requires Preparation

The Indian market represents one of the most significant growth opportunities available to Swiss businesses today. TEPA has created a preferential pathway that positions Swiss companies ahead of their European competitors. However, success requires more than just market opportunity – it demands sophisticated understanding of India's regulatory environment and proactive compliance management.

The companies that will thrive in India are those that invest in proper structure, maintain meticulous documentation, and treat regulatory compliance as a competitive advantage rather than a burden. For these companies, India offers not just a market but a platform for regional and global expansion.

The window of opportunity is open. The question is whether Swiss businesses are prepared to walk through it with the sophistication and preparation that success demands.

About This Analysis

This report is based on comprehensive analysis of the EY India webinar "India - What Swiss Cos need to know" conducted for the Swiss-Indian Chamber of Commerce, cross-referenced with current Indian tax regulations, Swiss Federal Tax Administration guidance, and recent legal developments. All tax rates and regulatory requirements have been verified against official sources as of September 2025.

Sources and Verification:

- EY Webinar: "India - What Swiss Cos need to know" (September 2025), hosted by the Swiss-Indian Chamber of Commerce

- PwC Tax Summaries: India - Corporate Taxes (accessed September 2025)

- Swiss Confederation, State Secretariat for International Finance (SIF): Switzerland-India Double Taxation Avoidance Agreement

- EFTA Secretariat: Trade and Economic Partnership Agreement (TEPA) between the EFTA States and India

- Grant Thornton Switzerland: Analysis of MFN clause suspension (December 2024)

- Indian Income Tax Department: Current tax rates and compliance requirements

- Swiss Federal Tax Administration: International tax treaty guidance

Legal Disclaimer: This analysis is provided for informational purposes only and does not constitute legal, tax, or investment advice. Tax laws and regulations are subject to change, and specific circumstances may affect the application of general principles discussed. Companies should consult qualified tax and legal advisors before making business decisions based on this analysis.